Appendix R: Recharge Supplemental Information

Accounting Treatment and Transactions

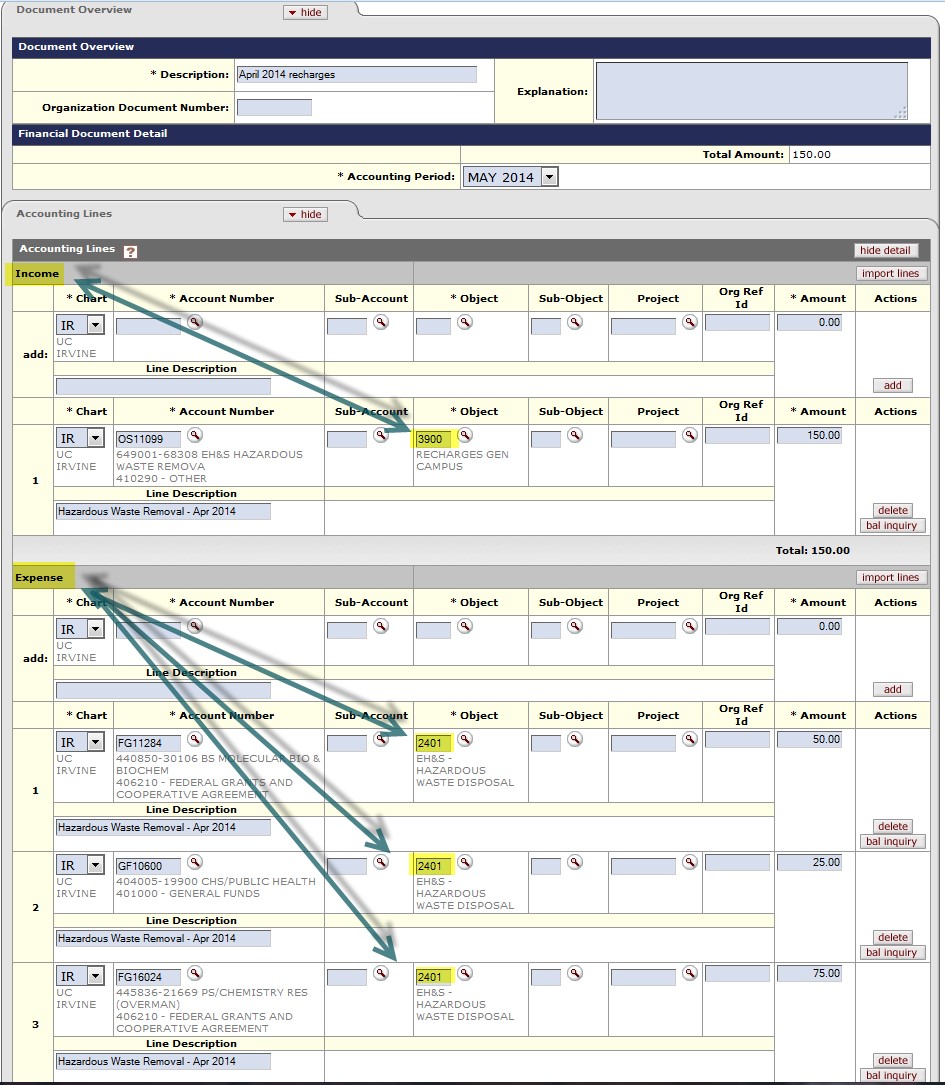

A recharge is an accounting operation to transfer expenditures associated with providing a good or service from one unit to another unit within the UC system. A recharge does not create or record revenue, but rather records a reduction of expense through the use of a contra-expense line item in the producing unit and an equal expense in the receiving department. The phraseology of the Kuali Financial System (KFS) indicates that a recharge entry is income (as illustrated below), but in reality, it is a contra-expense.

Through the development and approval process outlined in UCI policy Sec 701-22, a recharge facility will have a unique KFS Account (recharge account). The account number will be assigned by Accounting and Fiscal Services in the appropriate sub fund group. The recharge account is used to record both approved expenses associated with the delivery of a good or service and the corresponding (contra-expense) recharge.

In addition to a recharge account, a recharge facility may also have an associated subsidy account and/or a reserve and renewal account. Details for the use of these accounts are included below.

Expenditures to produce the good or service are recorded in a recharge account using appropriate expenditure classification object codes (salaries, supplies, etc.). The off-setting recharge appears as a credit to contra-expense object code 3900. In this fashion, when rolled together as a recharge account for reporting purposes, the expenses will be offset by the contra-expense entries and will have no residual surplus or deficit.

The recharge facility will be given a unique expenditure object code and that object code will be recorded in operating budgets of the unit receiving the good or service. (Note the illustration above, object code 2401 Hazardous Waste Disposal). See the published Official recharge list for all expenditure object codes.

For the Recharge Facility’s expenditure to produce a good or service:

- Debit: Expense in a Recharge Account, recharge operating fund (6xxxx), Appropriate exp object code

- Credit: Payment of the expense, Accounts Payable or Cash – not evident in the Recharge account financial reporting

For the recharge, transfer of expense to the receiving unit from Recharge Facility:

- Debit: expense in receiving unit’s KFS Account and debit object code (unique to the recharge facility)

- Credit: contra-expense in the Recharge Account, recharge operating fund (6xxxx), object code 3900

For transactions with non-university entities (Sales & Services Activities), a revenue object code should be used instead of contra-expense (please see Appendix S for more information).

Costing and Pricing

Not all costs for producing a good or service can be included in the calculation of a recharge rate and these costs should not be recorded in the recharge account. Section 2 CFR Part 220 (formerly Office of Management and Budget OMB Circular A-21), Cost Principles for Educational Institutions, defines direct and indirect (Facilities and Administrative-F&A) costs for purposes of accounting for federal accounts. Recharges are considered direct costs to those units receiving the good or service. These direct costs are defined as all readily identifiable costs associated with the furnishing of goods or services.

Given the sensitivity for accurately identifying costs for federal programs, recharges cannot include incidental administrative support such as clerical and secretarial assistance or minimal supervisory assistance that is not significant in time or dollar value, benefiting a single period. Costs incurred and assigned to the activity must be essential to the purpose for which the activity was established.

- Allowable Costs

- salaries and benefits of technical personnel directly related to the recharge activity

- supplies and reasonable general support costs (e.g., telephone charges and office supplies)

- equipment depreciation (straight line basis) and depreciation of capitalized improvements

- maintenance and repair costs (regularly recurring to keep property in an efficient operating condition and that are not capitalized). Multi year maintenance should be amortized with their annual amount.

- installation charges, and allowable lease and loan costs

- Unallowable Costs

- Training costs to create new goods/services are not allowed in the recharge account, because to do so would be charging users for services/goods not yet rendered

- Acquisition costs of inventorial equipment (however, depreciation of such equipment is allowed)

- Fees and stipends for undergraduate and graduate students

- Renovation costs that are capitalized

- Leasehold improvements

- Principal payments of capital leases

- Start-up costs are non-recurring costs necessary to prepare a new activity for its normal business purpose. Start-up costs may include both capital expenditures, such as those for equipment, and non-capital expenditures, such as moving expenses. Start-up costs that benefit more than one year must not be charged to the operating fund of the recharge activity. The start-up costs may be recovered through amortization. Generally, the amortization period should be five years or the number of years benefited by the cost.

- Payroll Costs

Payroll costs will be based on a reasonable estimate of productive hours, calculated as the annual number of hours per employee which can be directly attributed to the provision of goods or services. This excludes leave and holiday hours. The effective hourly labor billing rate would be the sum of salary and benefit costs to be recovered divided by the number of productive hours. - Pricing Methods

- Per unit rates are fully inclusive of all payroll, materials, depreciation, and other operating costs associated with a particular service or good. Such operating costs are divided by anticipated volume to determine the per unit rate. Rates will be stated in measurable units of goods or services.

- Hybrid pricing - hourly rate plus markup.

- Hourly rate is a type of per unit rate where the principal measurable unit is labor. It may be appropriate to set up an hourly rate for some services combined with a mark-up cost on materials or consumables that are highly variable for each service.

- Mark-up cost is an increase above the original purchase price of materials. In certain activities, a handling fee for the cost of materials is appropriate. The mark-up percentage is normally computed by dividing the total materials processing costs by the total materials cost. Materials processing costs usually consist of the salary and benefit costs of the person(s) involved in the ordering, receiving, etc. of materials, but could also include related costs such as computer, telephone, etc.

Interest

CFR Part 200 allows external interest costs to be included in the cost basis for development of recharge rates but does not allow for the recovery of internal interest (charges for the temporary use of internal funds). Care must be taken to ensure unallowable interest is not included in recharge rates or credited to equipment reserve funds (described below). Detailed restrictions are outlined in CFR Part 200.449.

Inventories

Guidelines for the maintenance and control of supply inventories as a recharge facility within the University (e.g. central stores, departmental storerooms, production facilities, etc.) are detailed in UC policy (Business & Finance Bulletin BUS-54). In order to provide effective service and to maintain high utilization of University resources, current policy indicates that inventory recharge accounts should be established "when the combined inventory value of new and unissued material in a department exceeds $50,000 at one or more locations on the campus or exceeds $50,000 at an off-campus location."

Specific requirements for central stores recharge activities are outlined in the directive. Generally, there should be a clear, net economic advantage to the university which more than offsets the cost of handling as a stores item or when the requisitioner's service requirement cannot be met by direct shipment from the supplier.

As with any recharge facility, the operating expenses of a store inventory are to be funded from a markup on the cost of goods sold and/or charges for services performed, so as to recover all elements of cost.

Subsidies

Sometimes a campus unit might wish to create a good or service for other campus units at a discounted cost. In these cases, another associated KFS Account, a Subsidy Account under the control of the unit must be identified. Funding for the subsidy must be identified and budgeted in the subsidy account and reference to the subsidy must be reviewed and approved as part of the recharge approval process.

A subsidy reflects costs that are not recovered through a recharge rate and that are contributed by the unit delivering the good or service. Subsidies are normally provided to keep the charge for a service lower than the full cost basis would require. Subsidies can be provided to cover general recharge expenses or may be used to cover specifically identified expenses. Subsidies may NOT be used to discriminate among recharge users without an acceptable justification. Subsidies can be provided in the form of:

- funds to support technical salaries and benefits of staff directly associated with the recharge activity

- funds for the purchase of equipment for use by the recharge activity

- funds to cover year-end deficits from the recharge activity operations

If an Official Recharge Rate is requested and approved that does not recoup the true costs of the activity, additional funding must be budgeted in a subsidy account that is clearly linked to the relevant recharge account. In the subsidy account, expenses should be recorded in the appropriate classification object codes. A subsidy account should be unique to the charge activity so that the amount of the subsidy for the recharge activity is clearly stated. If multiple recharge activities are subsidized by a unit, a singular subsidy account can be established with multiple subsidy sub-accounts: one for each activity. These sub-accounts will roll up to the subsidy account.

For example, if a unit has one recharge activity which requires a subsidy:

Recharge Account – SS12136 (UC Account 447418 and UC Fund 60103)

Subsidy Account – GF13377 (UC Account 447418 and UC Fund 19900)

In another example, the unit has multiple recharge activities which require a subsidy:

Recharge Account 1

Recharge Account 2

Recharge Account 3

Subsidy Account

Subsidy Sub Account 1

Subsidy Sub Account 2

Subsidy Sub Account 3

While no subsidies are included in the calculation of the recharge rate, the amount of the subsidy and the fund source should be evident and noted on Rate Calculation Worksheet for approval by the Unit’s Approving Authority.

Capital Equipment, Depreciation, and Transfer to Reserve and Renewal fund

Capital (inventorial) equipment items are standalone items with a useful life >1 year and value >$5,000. Capital equipment assigned to the recharge activity cannot be charged directly to a recharge account at the time of acquisition, but rather must be depreciated and expensed over the useful life of the asset. The depreciation expense should be included as a cost in the rate development and charged as expense to the recharge account, except as follows:

- Equipment funded by the Federal government or identified as cost sharing to a federal project.

- Equipment funded by an award under a private contract, where the contract is not completed. If the contract is complete and there is remaining life in the asset, the undepreciated balance remaining at the end of the life of the asset can included in the rate calculation. Example: asset has useful life of 5 years but 3-year life of the award, then asset may be depreciated for the remaining 2 years.

- Equipment Purchases - Equipment to be used in recharge activities can be purchased, through equipment reserve accounts (discussed below) or from institutional funds. Otherwise, an operating lease can be used to provide the necessary equipment. External loans or capital leases can be used to provide equipment; however, the debt repayment costs cannot be recovered fully through the recharge rate, only certain interest costs and depreciation of the equipment can be included in the rate. Given these limitations Deans’ offices may wish to modify their approach to subsidizing recharge centers by providing funding for equipment rather than salaries. An equipment reserve for recharge centers will be established with institutional funds that would be repaid through depreciation, similar to the working capital that has been available to some Recharge facilities.

- Depreciation Definition - Capital equipment cannot be fully expensed to the recharge account in the year of acquisition. Depreciation will be on a straight-line basis, charged annually over the life of the equipment, unless it can be demonstrated that some other method is more appropriate. The life of the equipment normally should be based on the UCOP useful life table. Depreciation costs are to be included as a cost element for rate determination purposes.

equipment or equipment purchased from unrestricted funds. Federally-funded equipment cannot be depreciated and cannot be included in the cost basis for internal customers. However, outside user rates can include the depreciation component in the rate. In this scenario, there would be two rates: 1) for internal customers (recharges) that does not include depreciation component in the rate; and 2) for external customers (sales and services income) that does include the depreciation component for federally funded equipment. - Recording Depreciation Expense - Transfer to Reserve and Renewal Fund - When equipment is depreciated through a recharge activity and included in the rate, the credit entries that are entered into the recharge account will (theoretically) be greater than the expenses that are debited to the account. The cumulative amount that is being credited to the recharge account that is attributable to the depreciation, must at year-end be transferred out of the recharge account and into a separate reserve and renewal fund (76xxx). Recharge activities with depreciable equipment must contact General Accounting to request that depreciation expense be recorded via a financial journal (BAC) that will debit the recharge account and credit a reserve and renewal fund. The BAC document will also move cash into the new reserve funds though this aspect of the journal entry will not be evident to the unit.

Justification demonstrating the accumulated depreciation in the recharge account will be required and no surplus funds will be transferred. The request should be submitted to Accounting before the close of Period 12.

The following are the financial entries (evident to the unit) to record depreciation expense and to transfer funding to the equipment replacement fund:- Debit (-): KFS Account, recharge operating fund (6xxxx), Object code X500

- Credit (+): KFS Account, R&R fund (76390), Object code C050

- Use of the Reserve and Renewal Account - Through the entries above, an equipment replacement reserve account is established. The equipment replacement reserve (account RRXXXXX) should be used to support the future replacement of expended assets needed for the recharge operation. Use of the equipment replacement reserve account for other recharge unit expenses is by exception only and subject to approval. Requests for alternate uses of equipment reserve funds may be sent to the appropriate decision maker or Dean’s Office and should describe the proposed use of the reserve account, including the dollar amount to be used. The request should also discuss the unit’s future capital needs and how they will be met in the absence of a fully funded equipment replacement reserve. The approved request should be forwarded to the Accounting Office for review and approval.

A decommissioned recharge unit may use its equipment replacement reserve fund to offset any recharge operational deficit. Balances in the reserve fund beyond deficit coverage may be retained by the department.

Surplus/Deficit

Recharge activities will be operated on a no-gain/no-loss basis. Any surplus or deficit occurring in any one year will be corrected by adjustment of rates in the succeeding year to achieve a break-even balance at the succeeding year end. Every effort should be made to ensure that year-end surpluses or deficits do not exceed Two month of the recharging unit's expenses. The adjustment of rates will generally be based on estimates since actual performance data for the year will not be available prior to the development and publication of the succeeding year's recharge rates. In exceptional cases when such an adjustment would create a severe fluctuation in rates from one year to the next, achievement of a break-even balance can be extended for a reasonable period beyond the succeeding year upon approval by the Recharge Rate Review Committee.

As part of the annual recharge rate review, units that carry an unacceptable deficit are required to explain a deficit situation and corrective action that will be taken to eliminate it.

If a unit does not make discernible improvement on the deficit by the end of the 4th quarter following the annual review, the coordinating point will be notified at the end of July and the unit required to submit a deficit reduction plan by the end of August.

The deficit reduction plan must include a narrative and supporting financial analysis that details how the deficit will be reduced to acceptable limits by the end of the fiscal year.

If the deficit is not reduced to acceptable limits in that timeframe, the coordinating point must cover the deficit.

How to Close an Activity

Within 10 days of deciding to close a recharge operation, please email your Coordinating Point/Dean’s Office and the Recharge Committee (campusrecharge@uci.edu), advising of your decision. In addition, please advise when the operation will close and how you intend to account for any remaining surplus or deficit. On receipt of this information, we will make all appropriate changes to the recharge web site.

When a recharge unit ceases to operate, the remaining balance must be treated as follows: For surplus balances - If the surplus is > 1 months operating costs, the balance will be refunded back to the unit’s recharge customers on a pro-rata basis, within 30 days of closure. The refund will be allocated on the basis of charges made to these customers in the last 12 months. If the surplus < 1 months operating costs, the balance is retained by the sponsoring unit and moved to an appropriate account.

For deficit balances - If the unit closes with a deficit balance, the balance must be transferred financially to an appropriate account within the department. If it is not moved by the fiscal year’s end, the entire deficit balance will be subject to the terms of the deficit policy without the application of a tolerance. A decommissioned recharge unit may use its equipment replacement reserve fund to offset any recharge operational deficit. Balances in the reserve fund beyond deficit coverage may be retained by the department with Accounting and Fiscal Services’ approval.